Smart Grid Market Share Competition Intensifies Among Platforms Metering And Automation Vendors

The Smart Grid Market Share landscape is shaped by long utility procurement cycles, multi-year modernization programs, and the convergence of metering, automation, and software platforms. Market share often concentrates among vendors that can meet utility-grade reliability, cybersecurity, and interoperability requirements. Advanced metering infrastructure deployments can be large and long-lived, giving winners significant installed-base advantage for subsequent analytics and customer programs. Distribution automation vendors compete on device reliability, communications integration, and restoration performance. Software platform providers compete on ADMS, OMS, and DERMS capabilities, where integration breadth and usability are decisive. Market share is also influenced by regional standards, regulatory requirements, and local manufacturing preferences in critical infrastructure procurement. Utilities frequently favor vendors with proven field performance and strong support networks, because outages and failures carry high public and regulatory costs. As DER and EV integration accelerates, vendors that offer strong orchestration and analytics capabilities can expand share by becoming central to utility operations.

Ecosystem partnerships influence share dynamics. Systems integrators often shape vendor selection by designing architectures and managing multi-vendor integration. Telecom and connectivity partners affect AMI deployments through RF mesh, cellular, or private LTE networks. Vendor ability to integrate with existing GIS, asset management, and legacy SCADA systems often determines success. Utilities also value roadmaps that support standards and interoperability, reducing lock-in risk. Market share shifts can occur when utilities prioritize cybersecurity modernization, favoring vendors with mature security controls, certifications, and OT incident response capabilities. Performance during major storm events can also influence reputation and renewal decisions. Vendors that deliver proven reductions in outage duration and improved situational awareness can expand within accounts. Conversely, vendors with upgrade instability or integration failures can lose share as utilities standardize on fewer strategic partners. Managed services are another share driver; some utilities prefer vendors that operate platforms under SLAs, especially where internal staffing is limited. This can consolidate share with service-oriented providers that offer end-to-end programs.

Technology innovation will continue influencing market share. Vendors that support edge intelligence, predictive maintenance analytics, and integrated DER orchestration can gain share as grid complexity increases. EV management capabilities may become a key differentiator, including managed charging, transformer loading analytics, and customer program integration. Cloud and hybrid deployment options can influence share as utilities modernize data platforms and analytics. However, many utilities remain cautious about cloud for critical operations, so vendors must provide clear security and resilience assurances. Interoperability remains crucial; utilities often operate equipment for decades, so vendors that support open standards and flexible integration can retain share longer. Pricing models and total cost of ownership also influence share, including software licensing, maintenance contracts, and device lifecycle support. Utilities increasingly evaluate vendors on outcomes, such as SAIDI/SAIFI improvements and reduced operational costs, rather than on feature lists alone. Vendors that can quantify and validate these outcomes through analytics and case studies gain advantage.

Future market share shifts may include consolidation and platform convergence. Larger vendors may acquire niche DERMS, cybersecurity, or analytics firms to broaden offerings and capture more of the modernization spend. Utilities may consolidate vendors to reduce integration complexity, which can concentrate share among platform leaders. However, regulatory and risk teams may encourage multi-vendor strategies to reduce dependency. Regional policy and supply chain sovereignty requirements may support domestic vendors in some markets. Market share winners will be those who combine trusted field hardware with strong software orchestration, robust cybersecurity, and reliable lifecycle support. As smart grids become the backbone for electrification and decarbonization, vendors will be judged by operational performance under stress—storm response, cybersecurity resilience, and the ability to integrate distributed resources safely. For utilities, strategic vendor selection will increasingly focus on long-term partnerships, interoperability, and measurable reliability improvements that justify continued investment and public trust.

Top Trending Reports:

Mobile Collaboration Productivity And Innovation From Workplace Market

Categorias

Leia Mais

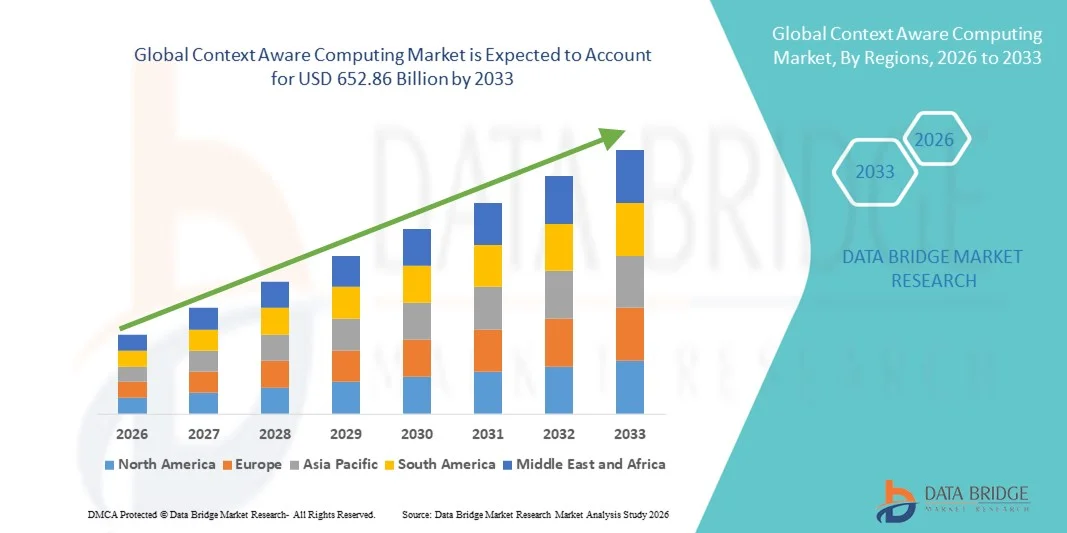

"Executive Summary Context Aware Computing Market Market Size and Share Forecast The global context aware computing market size was valued at USD 77.9 billion in 2025 and is expected to reach USD 652.86 billion by 2033, at a CAGR of 30.44% during the forecast period This Context Aware Computing Market Market Research Report also conducts analysis on...

Buy GitHub Accounts Buy In the fast-paced world of tech and software development, having a strong online presence is essential. Enter GitHub, the platform where millions of developers showcase their work, collaborate on projects, and contribute to open-source initiatives. But did you know that purchasing GitHub accounts can give your business an edge? Whether you’re looking to expand your...

Introduction The digital world has transformed the way businesses operate and communicate with customers. Today, having a professional website is no longer optional for companies that want to grow in competitive markets. “Website development” plays a major role in creating online platforms that help businesses showcase products, provide services, and connect with customers...